December is make-or-break for Mother Jones’ fundraising. We have a $350,000 goal that we simply cannot afford to miss. And in "No Cute Headlines or Manipulative BS," we explain, as matter-of-fact as we can, how being a nonprofit means everything to us. Bottom line: Donations big and small make up 74 percent of our budget this year and are urgently needed this month, and all online gifts will be matched and go twice as far until we hit our goal. Please pitch in if you can right now.

December is make-or-break for Mother Jones’ fundraising, and in "No Cute Headlines or Manipulative BS," we hope that giving it to you as matter-of-fact as we can will work to raise the $350,000 we need to raise this month. Donations make up 74 percent of our budget this year, and all online gifts will be matched and go twice as far until we hit our goal.

Narayana Kocherlakota thinks the Fed needs to respond to the coronavirus pandemic by reducing interest rates:

The outbreak has triggered a huge burst of risk aversion in financial markets. We should expect that risk aversion to manifest itself as a drag on household and business spending on travel and many other services. There is, of course, the possibility that this risk aversion continues to grow, creating its own negative dynamic: As consumers and businesses respond to alarming events, they pull back, causing growth to slow still more.

This cycle is why the economic threat from the virus is so unnerving. If the cycle develops, it would represent an adverse demand shock that will weigh on businesses’ willingness to hire and raise prices. The appropriate monetary policy response, of course, is to ease interest rates.

I think Kocherlakota is right—though perhaps not for the reason he outlines. At this point, we still don’t know how strongly the coronavirus outbreak will affect the US economy. It’s unclear if rate cuts are appropriate yet, and under normal circumstances I might favor waiting a bit longer before making a decision.

However, even before the outbreak there was a good case to be made for at least a modest reduction in interest rates. So even if the coronavirus outbreak turns out to have only a small effect on the economy, a rate cut is probably a good idea anyway. The added benefit of demonstrating that the Fed is willing to deal aggressively with a public health emergency is just gravy.

So yes: cut interest rates soon. The upside might be high and the downside is almost certainly low.

For some reason I’ve recently seen a little spate of skepticism over the notion that middle-class incomes have been stagnant for quite a while. I suppose this is a reaction to Bernie Sanders, who certainly has a habit of making things sound a little more catastrophic than they really are. But that’s no reason to doubt the basic fact of income stagnation—at least for some people.

Here are the figures from the Census Bureau for men of different ages:

Since 1980, the income of every men’s age group has declined except for those 55-64—and even that age group has been stagnant since 2000. Now here are women:

Women’s incomes have been rising steadily, though they’re still considerably lower than men’s incomes.

Now, this is cash income and doesn’t include government benefits. And it uses CPI-U-RS as its inflation gauge. You can get different results if you calculate income differently or if you use a different measure of inflation. However, cash income is best if you’re interested in how people view their own financial situation, since most people don’t include benefits when they think about how well they’re doing. And I happen to think that CPI-U-RS is the best inflation measure we have.

So if you want to know how people view their own financial situation, these charts are a pretty good indicator. Middle-class men of prime working age have been on a slow downward slide for 40 years, and an even steeper slide since 2000—though gaining back a bit over the past five or six years. Middle-class women, by contrast, have been gaining steadily but still make way less than men.

In other words, just about everyone has good cause to be frustrated and unhappy. That’s especially true since the affluent have been doing so well during the same period. Frankly, it’s sort of a miracle that people aren’t more pissed off than they are.

You may have noticed that looking at old digital photos is like going through a technological time machine: the older the photo, the lousier the quality. So today let’s go back to the very beginning. On my birthday in 1997 Marian got me a Sony Mavica, one of the first consumer digital cameras. It created pictures with a resolution of 320×240 and stored them on a floppy drive. This one, titled “Still Life With Fritos,” is from the very first floppy disk of images that I took.

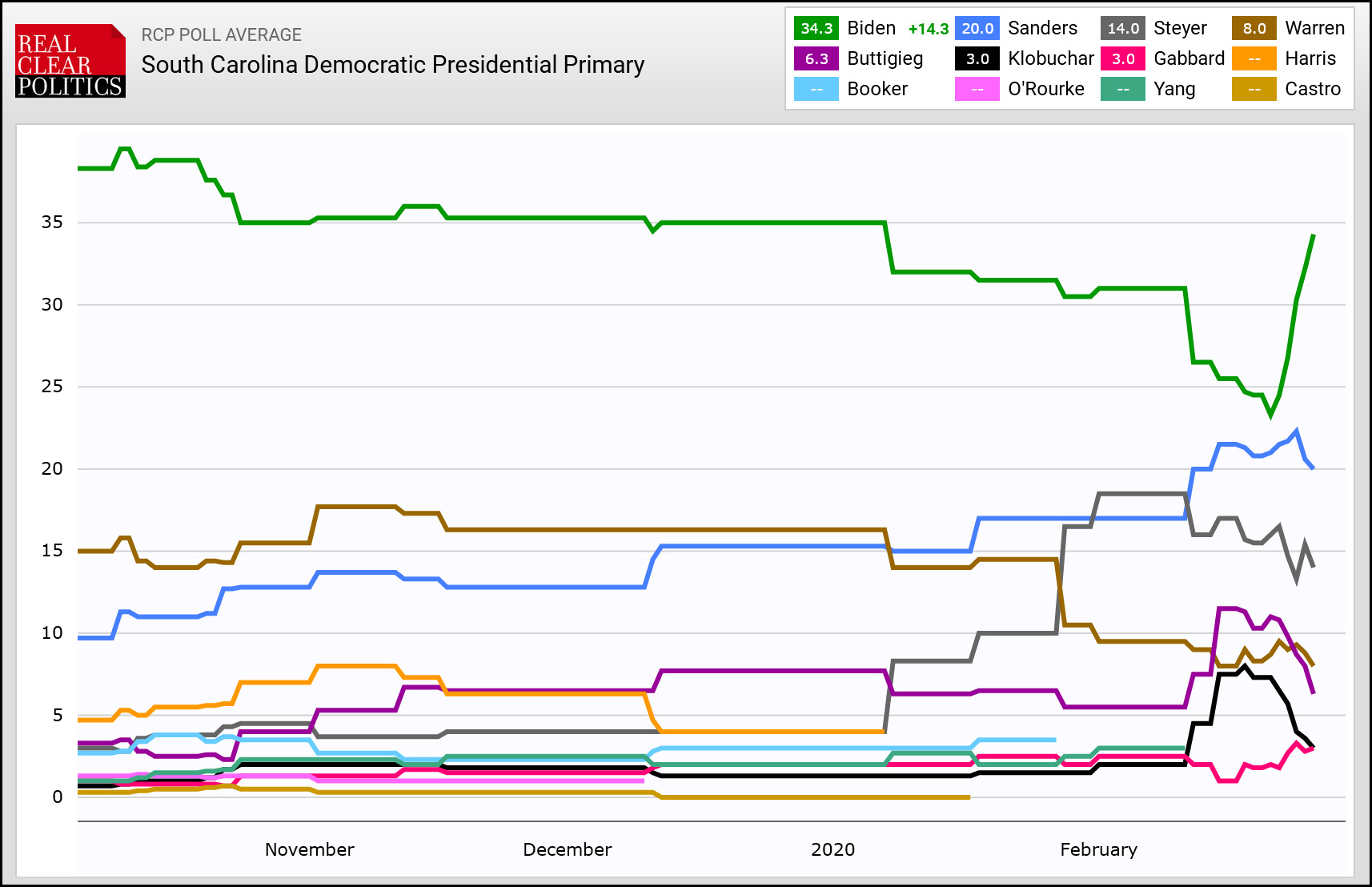

In national polls, the best you can say about Joe Biden is that he’s no longer plummeting. But in South Carolina, the past week has been a terrific one for him. According to the Real Clear Politics aggregate, he’s made up all the ground he lost earlier in the year:

This is quite the exciting Democratic primary, isn’t it? If Biden pulls off a solid win in South Carolina it could have a big effect on Super Tuesday.

Matt Yglesias points out today that a Swedish paper about lead poisoning in children has finally been accepted for publication, and this gives me an excuse to republish what I wrote a few years ago when it was still a working paper. Here it is.

Just as in the US, Sweden phased out leaded gasoline in the 70s and 80s, which caused lead poisoning in infants to decrease. Unlike the US, however, lead levels were already fairly low, so the Swedish team was able to measure the effect of changes not just from 30 ug/dl to 20 to 10, but from 10 to 5 to 2. What they found was that the impact of lead reduction does eventually flatten out, but it happens at very low levels. There are gains to be made by reducing blood lead levels all the way down to 2-3 ug/dl.

At the risk of some slight irresponsibility, however, I want to reproduce their chart for violent crime. Here it is:

This might mean nothing, since the error band is quite large. But if it’s right, there’s no threshold for lead poisoning and violent crime. Just the opposite, in fact. As childhood lead levels decrease, the likelihood of violent crime later in life decreases all the way down to about 6 ug/dl. Then, after flattening out, it takes a sharp downward dive starting around 2 ug/dl. In other words, getting that last little bit of lead out of the environment might pay off considerably in less violent crime 20 years from now.

Because of the large error bars, this is the kind of thing that needs confirmation. But it would be worth the effort. We already know that reducing lead levels from 30 to 20 to 10 to 5 pays off, but we don’t know very much about levels below that. It could be that anything under 5 ug/dl is OK. Alternatively, the difference between 5 ug/dl and 1 ug/dl might be considerable. Or, given the error band, the effect could be linear all the way down. We should find out.

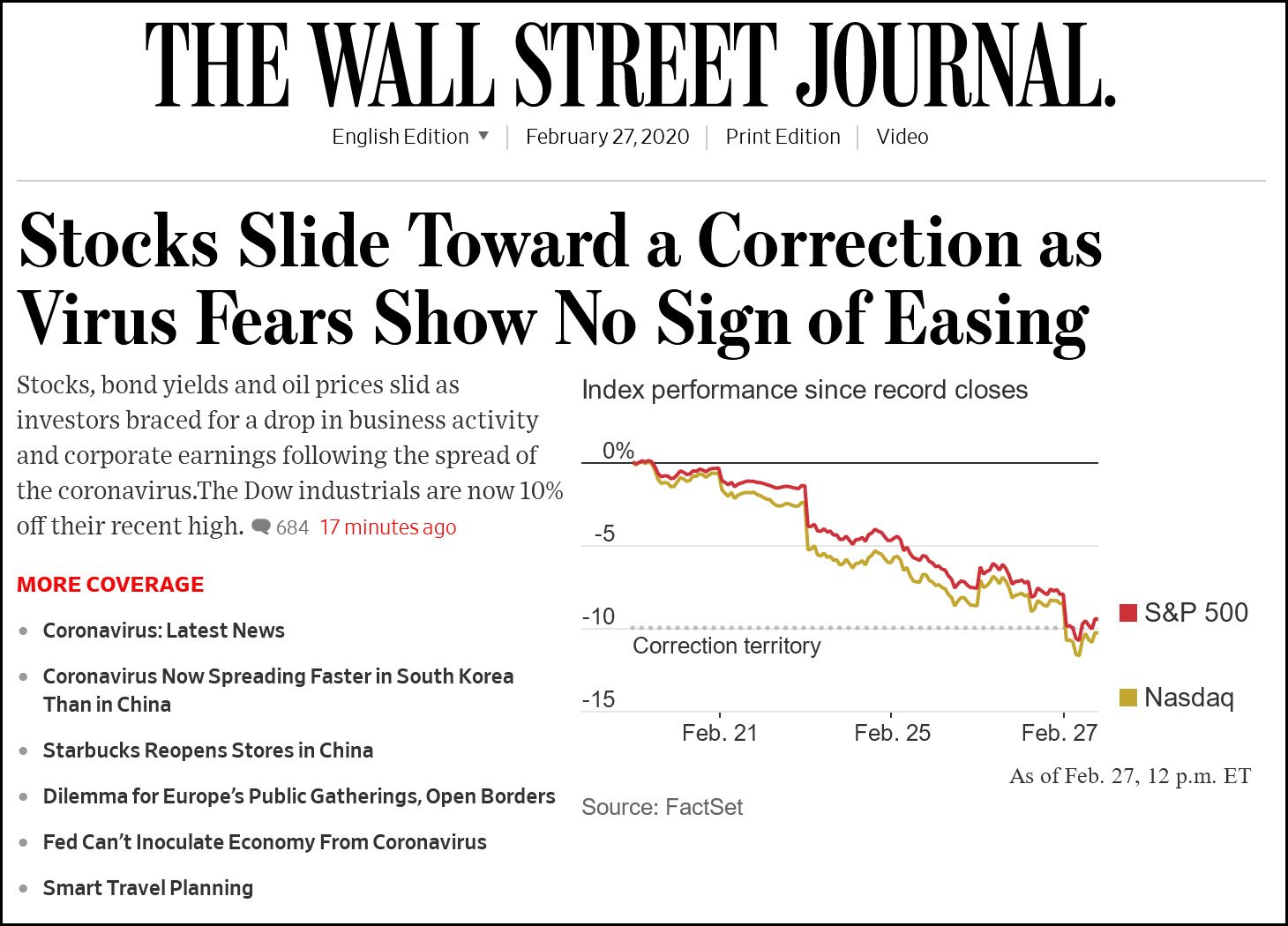

Yesterday I mocked President Trump for being more concerned with the stock market than with the coronavirus. I stand by that, but it’s hard to blame him too much when I wake up to headlines like this:

Sure, you say, but that’s the Wall Street Journal. They’re supposed to be obsessed with the stock market. But here’s the New York Times:

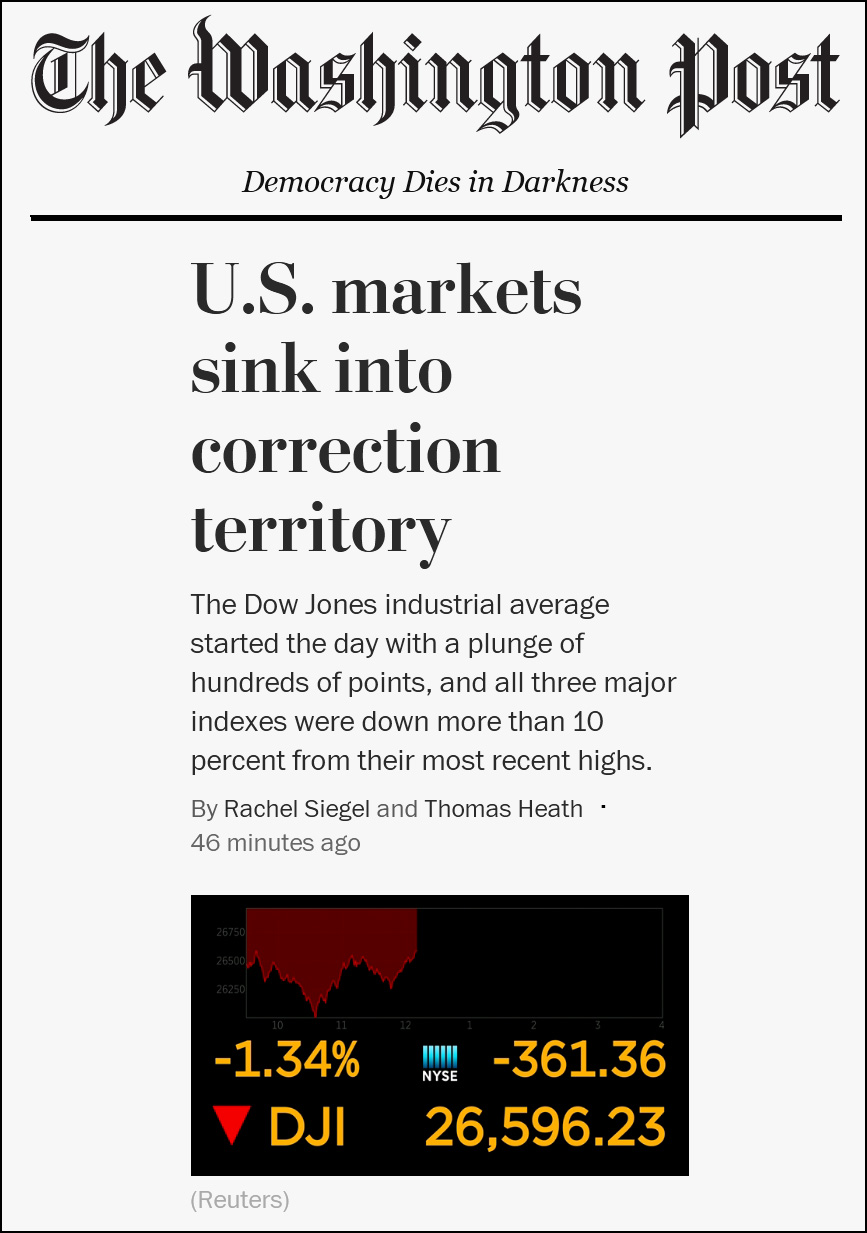

And the Washington Post has a live feed so you can watch the stock market crater before your eyes:

I could forgive this infatuation with the stock market if it was connected to some actual change in the broader economy, but it’s not. It’s handy only because most economic indicators are calculated monthly at best, and that’s boring. The stock market may not have much to say about the real-life state of the economy, but it changes daily—hourly, even—and that makes it exciting.

But that’s no excuse. A serious piece about how the coronavirus is likely to affect the global economy is fine. But stock porn? Spare me.

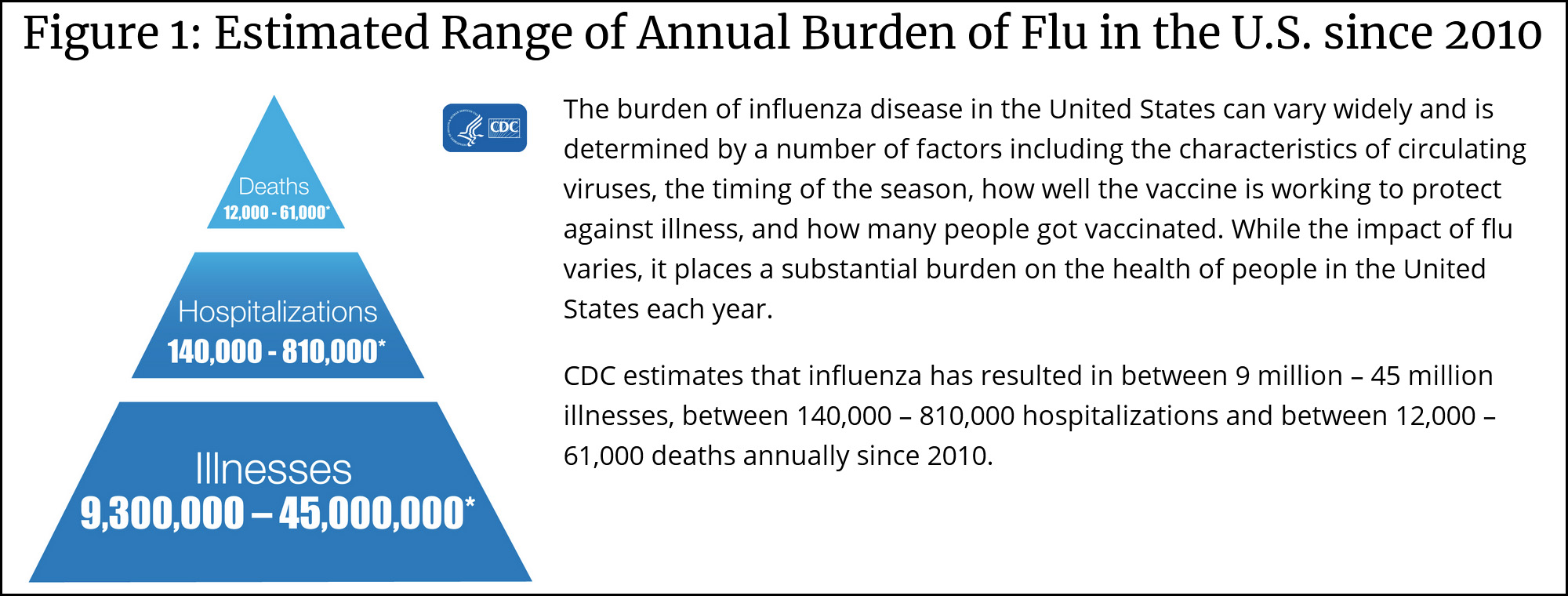

Just in case you’re curious, it’s true that the mortality rate of the COVID-19 virus is about 2 percent so far. However, it’s not true that this is the same mortality rate as the flu. In the United States, here’s the CDC’s estimate:

This comes to about 0.13 percent, a small fraction of the COVID-19 mortality rate. But be careful, get vaccinated, and wash your hands anyway.

This is a pair of ravens against a background of classic Arizona red rock country. It was taken a few miles away from the south entrance to the Grand Canyon.

I’d personally say that color is important to this shot since this is, in fact, red rock country. However, I also have a black-and-white version at the bottom. You can decide for yourself which you like better.

Trump is highly concerned about the market and has encouraged aides not to give predictions that might cause further tremors….In a Twitter post, he misspelled the word “coronavirus” as “caronavirus” and wrote that two cable news stations “are doing everything possible to make the Caronavirus look as bad as possible, including panicking markets, if possible. Likewise their incompetent Do Nothing Democrat comrades are all talk, no action. USA in great shape!”

….Privately, Trump has become furious about the stock market’s slide, according to two people familiar with the president’s thinking, who spoke on the condition of anonymity to share internal details. While he has spent the past two days traveling in India, Trump has watched the stock market’s fall closely and believes extreme warnings from the Centers for Disease Control and Prevention have spooked investors, the aides said. Some White House officials have been unhappy with how Health and Human Services Secretary Alex Azar has handled the situation, they said.

The good news, I guess, is that at least Trump is concerned about something. Eventually, he might decide that happy talk won’t save his bacon and he actually needs to do something substantive about the spread of the virus. The big questions are (a) how long this will take and (b) whether he can find someone competent to run this effort. I can’t think of any previous president that I’d be worried about on this score, but there you have it.

Trump has a simple—and surprisingly effective—approach to marketing: When someone else is in charge, everything is in terrible shape. When he’s in charge, everything is perfect. This is fairly benign when it applies to things that Trump has no control over—which is nearly everything—but not so benign when it interferes with things that Trump really does need to address. That’s what’s happening now. On the bright side, at least he hasn’t yet appointed Jared Kushner as our new coronavirus czar.

In these days of coronavirus anxiety, it’s important to greet strangers in the safest way possible. Short of adopting the Japanese bow, it turns out that the fist bump is our best bet. In fact, perhaps we’ll now evolve to new versions of the fist bump that become progressively lighter until they stop just short of actual skin contact. Perhaps our germaphobe president can lead the way?

Can you pitch in a few bucks to help fund Mother Jones' investigative journalism? We're a nonprofit (so it's tax-deductible), and reader support makes up about two-thirds of our budget.

We noticed you have an ad blocker on. Can you pitch in a few bucks to help fund Mother Jones' investigative journalism?

Billionaires own the media, but they don’t own us.

At Mother Jones we know these aren’t conventional times, and they require unconventional coverage. That’s what we deliver every day: fierce, independent journalism you can’t find elsewhere. Perhaps never in the history of our country has that been more necessary than now. But we can’t do it without reader support—your support. Please chip in today.

Billionaires own the media, but they don’t own us.

At Mother Jones we know these aren’t conventional times, and they require unconventional coverage. That’s what we deliver every day: fierce, independent journalism you can’t find elsewhere. Perhaps never in the history of our country has that been more necessary than now. But we can’t do it without reader support—your support. Please chip in today.