A reader emailed this morning asking for a really basic primer on Obamacare and the repeal effort. Judging from some of the stuff I’ve read, this sounds like a good idea. What follows is really basic, so skip it if you already know this stuff.

1. The insurance market

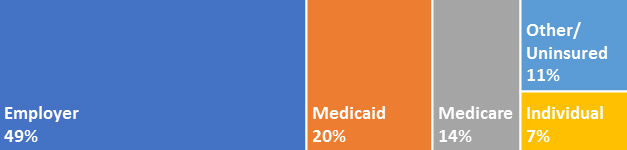

Most of us get our health insurance either from our employer or from Medicare. Neither Obamacare nor the Republican health care bill affect either one except in a few minor ways. They deal solely with two other parts of the health insurance market: Medicaid and individual insurance. Everything you hear about exchanges, premium increases, death spirals, and so forth applies to individual insurance only, which is a tiny piece of the entire market. It’s the little yellow box on the far right:

Yesterday the New York Times ran a piece saying that recent premium increases had affected “only” 3 percent of Americans. Technically that’s true, but it’s pretty misleading. That’s half the individual market.

2. How is Obamacare working out?

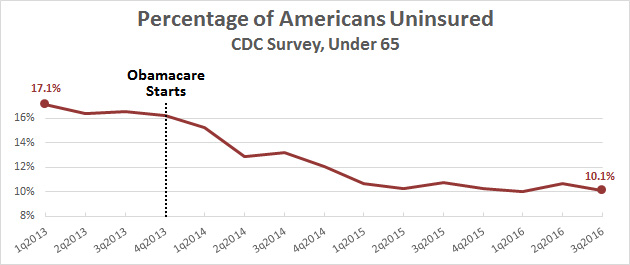

The main goal of Obamacare was to reduce the number of people who are uninsured. It did this two ways. First, it expanded Medicaid, which now covers about 10 million more people than before. Second, it set up the exchanges, where private insurers could sell individual coverage. This also covered about 10 million additional people. Altogether, Obamacare has substantially reduced the number of Americans who lack health insurance:

This isn’t to say that Obamacare has been perfect. Insurers misjudged pricing early on, which led to large premium increases last year as they finally caught up. The individual mandate wasn’t strong enough, so lots of young, healthy people have avoided insurance altogether, which makes the total pool covered by the exchanges older and sicker than originally predicted. As a result, several insurers have left the market, and there are lots of counties where only one insurance company is still selling in the exchanges.

3. How does Obamacare work?

Medicaid is simple: Obamacare simply allocates more money to cover more people. However, states can decline the expansion, and many red states have.

The exchanges are a little more complex and rest on three pillars. First, no one can be turned down for insurance because of pre-existing conditions. However, this means the number of sick people in the insurance pool will increase, and that needs to be balanced with healthy people. So the second part of Obamacare is the individual mandate, which requires everyone to buy insurance. If they don’t, they have to pay a tax penalty. But you can’t very well require poor people to buy something they can’t afford, so the third part of Obamacare is subsidies, which help reduce the cost of insurance for the poor and working poor.

4. How is Obamacare paid for?

Basically, by some modest taxes on the rich along with some taxes on corporations. Here’s the CBO’s latest estimate:

Overall, Obamacare helps the deficit because its taxes are a bit higher than its outlays, which have been less than projected. The Republican bill has no revenue sources yet. We don’t know how much it would cost, but whatever it is, the number will go straight onto the deficit.

5. Can Republicans repeal Obamacare?

This is tricky. Democrats can filibuster any repeal bill, and Republicans don’t have 60 votes in the Senate to overcome a filibuster. That means they have to repeal Obamacare via reconciliation, which requires only a simple majority in the Senate.

But there’s a big problem with reconciliation: it can be used only on things that directly affect the federal budget. Subsidies affect the budget, so Republicans can repeal the subsidies. Medicaid expansion affects the budget, so they can repeal that. The individual mandate affects the budget, so they can repeal that.

But there’s something missing here: the pre-existing conditions provision. That affects only insurance companies. It has no effect on the federal budget, so the pre-existing conditions ban can’t be repealed. Besides, the ban is extremely popular, so it would be political suicide to repeal it. This is a big problem: if insurers are required to insure everyone, even people with expensive pre-existing conditions, they’ll go bankrupt unless healthy people also sign up. But with skimpy subsidies and no individual mandate, the number of healthy people is going to plummet. This is going to leave insurers with a pool of people whose premiums are far lower than the cost of their medical care, and that in turn means insurers will lose tons of money. It’s a disaster waiting to happen.

6. So what will Republicans do?

Your guess is as good as mine. One option is that they just bull ahead without worrying about the consequences, and the individual market will implode. Another is that a few Republican senators see reason, and the repeal effort fails. A third possibility is that the repeal bill passes, and then Republicans count on Democrats helping them out with subsequent bills to fix things, because Democrats don’t want to see the entire individual market go up in smoke. Finally, a fourth option—which is very unlikely—is that Republicans increase the subsidies and tighten up the mandate, which will keep the individual market in decent shape.