Get your news from a source that’s not owned and controlled by oligarchs. Sign up for the free Mother Jones Daily.

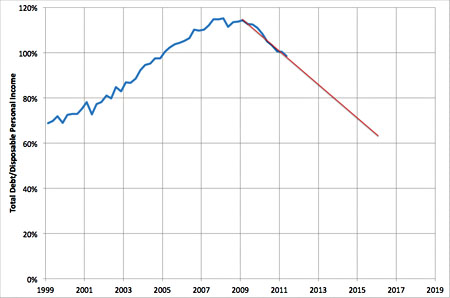

Via Stuart Staniford, here’s a chart showing the latest figures for total outstanding household debt as a percent of disposable personal income. Bottom line: American families are still heavily overleveraged, and it doesn’t look like we’re going to get back down to pre-bubble levels until 2015 or 2016. Stuart’s conclusions:

- US household deleveraging is a slow, painful, but orderly process.

- It’s likely to continue for a number of years more.

- It’s a drag on growth but is not going to cause the end of the world as we know it.